Updated January 2022.

The 529 college saving plan was introduced in 1996. So, the first generation to benefit from it now gets to use it for their own children. For those who are not familiar with the 529 plan, it’s a simple, flexible way to pay for college. And that’s a pretty big deal!

What the 529 Plan Does Today

The 529 plan lets you shelter from taxes the money you save to pay for your children’s educations. That shelter is similar to a what happens in a Traditional IRA. This is a big deal for a couple of reasons.

The first is that earnings inside a 529 plan account are allowed to grow without anything getting siphoned off to federal taxes.

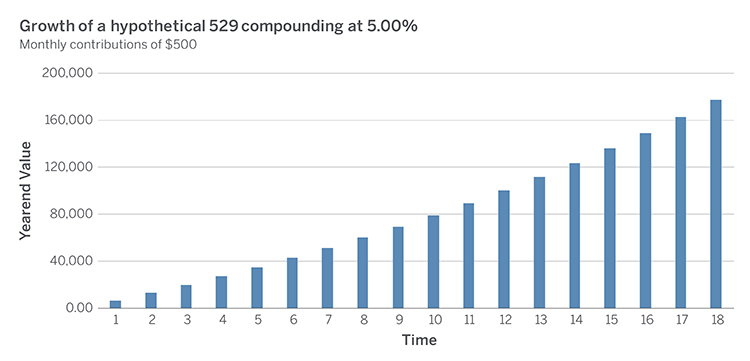

Here’s an example. Let’s say you open a 529 plan account today. You put $500 a month into it. You keep that up for 18 years.

Assume the account earns an average annual return of five percent, you know, nothing extraordinary. Now consider that you’ll lose nothing to taxes. Doing this could provide your college-bound kid with upwards of $177,000 to pay for school.1

Assume the account earns an average annual return of five percent, you know, nothing extraordinary. Now consider that you’ll lose nothing to taxes. Doing this could provide your college-bound kid with upwards of $177,000 to pay for school.1

What the 529 Plan Does Down the Road

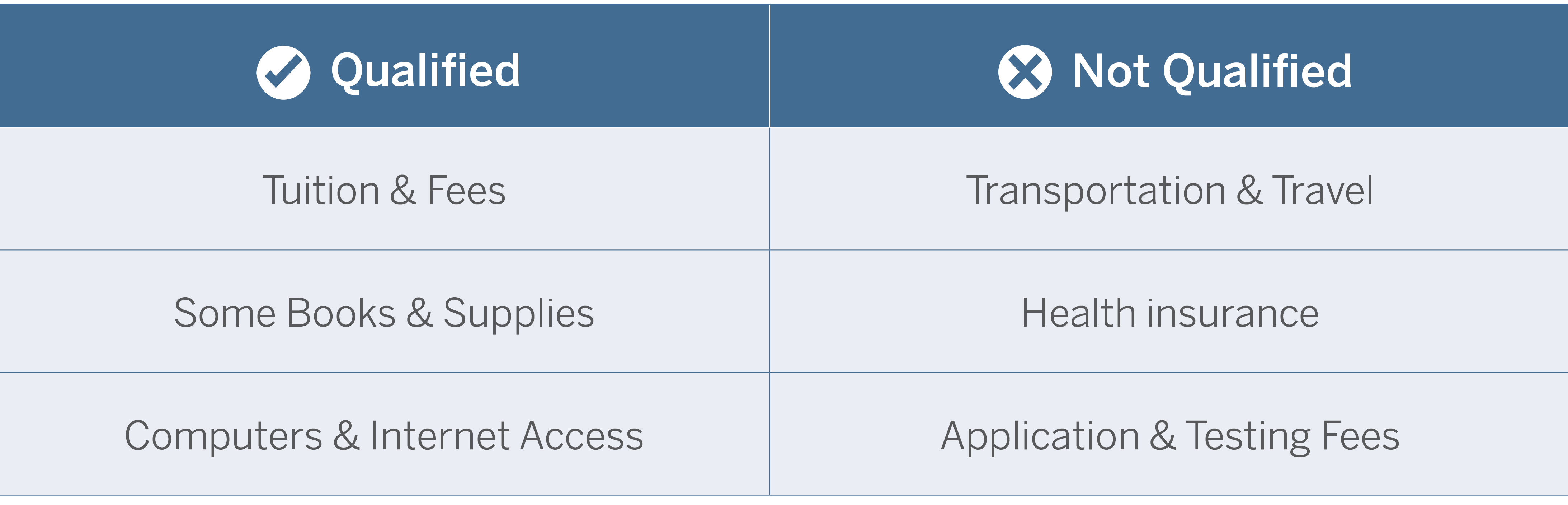

The second tax break the 529 plan account offers is that money coming out of it doesn’t get taxed as income to either you or your child. But there’s a catch. Those withdrawals have to be used for qualified education expenses.

Qualified education expenses are anything required for enrollment or attendance. So, for example, a computer and internet access to do assignments typically makes the cut. A bike to get to class on time doesn’t.

How much to Contribute to a 529 Plan

A general rule of thumb is to contribute no more than your kids will actually need to pay for school. But depending on state that runs the plan, contributions limits can be huge! For example, New York’s lifetime ceiling is $520,000.2

Whatever you contribute, just consider that the federal gift tax exclusion is $16,000. Any contributions over that are subject to gift tax. Still, this means a couple could contribute $32,000 per year per child into 529 plan accounts (oh, and don’t forget about grandparents).

Also consider that in some states, 529 plan contributions may be deductible for state income tax purposes.

529 Plans are Simple and Flexible

Many states offer two types of 529 plans, Prepaid Tuition Plans and College Savings Plans.

Prepaid tuition plans let you prepay future tuition at today’s rates, regardless of the future cost when your kids actually attend. The money typically can only be used for tuition at specific institutions in that state.

College savings plans, however, can be used at any eligible institution that participates in American federal student aid programs.

Who Controls the Money

The person who opens and funds the account is the owner. This is important because the account owner controls the money. Your kids don’t have access to it.

Now, if they decide to not attend college, there are options. You can change beneficiaries or even use the money yourself to attend cooking classes in Italy. There are restrictions, but there’s lots of flexibility.

And if you need help determining if your savings plan is on track, our College Savings Calculator can help you estimate costs to fill any funding gaps. Or call us at (800) 235-8396.

1 This hypothetical illustration is not indicative of actual returns on real investments. It is intended to demonstrate how compounding works. Your actual results will vary based on the real-world inputs of your unique financial circumstances. You should seek the advice of a qualified professional financial advisor.

2 Source: New York's 529 College Savings Program Direct Plan.