Do you ever feel uncertain about your investment decisions? Like you second guess yourself every time you contemplate making a move. To get some level of predictability into your long-term investment returns it helps to understand what’s driving them. Portfolio risk and return aren’t completely random. They’re a bit more predictable than you might think.

The long-term return your portfolio is likely to generate is mostly dependent on one critical component, your asset allocation. Research shows that it’s the primary influencer of portfolio return.1

The assets in your portfolio help explain what its expected return will be and how much risk you might take to achieve it. How you structure your long-term investment mix has a huge influence on future returns.

This is because assets like stocks, bonds and cash don’t behave the same way. They don’t have the same types of risks or returns. What they do have in common is a long history of documented results.

Predictability vs. Reliability

People often joke that predicting stock market returns is only possible for those with a crystal ball. But you don’t need magic to predict long-term portfolio returns. You just need math, specifically statistics.

The range of risks and returns of various asset classes may be different, but they are also statistically reliable. Over long periods of time, they generally fall within easily identifiable parameters. They may be erratic in the short run, but they are only very rarely off the charts.

Their long-documented history also makes them statistically valid. And there’s enough past information to reasonably conclude that their future numbers will probably be grouped within those same parameters. However, future results could vary greatly from what we have seen in the past.

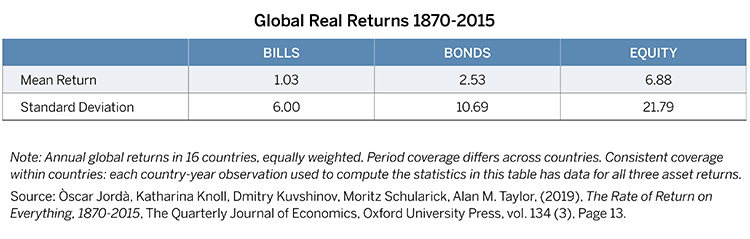

There’s plenty of research out there that documents the mean return and risk (expressed as standard deviation) of every imaginable type of investment.2

Mean return is used to calculate expected return and standard deviation defines ranges of return. But it’s important to note that standard deviation doesn’t define the full range of possible returns. This is especially important to understand when considering stock investments. Stocks can move wildly higher or lower than standard deviation suggests. They can produce negative returns in some cases. This volatility is what makes stocks risky.

So, estimating future investment risk and return is all about probability. What’s the chance the future might look something like the past? While not perfect, it’s a lot more reliable than winging it.

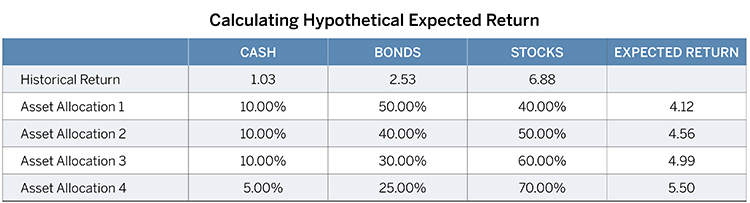

Since investable assets all have defined ranges of expected return, mixing them together helps define a portfolio’s combined expected return. This is what asset allocation is all about.

Asset Allocation and Expected Return

Using a baseline assumption for risk and return numbers, you can construct model portfolios to estimate future risk and expected return over time.

Asset allocation can’t predict your specific investment returns. But it is a very useful starting point to help you see if you’re headed in the right direction. Expected return can be used to calculate theoretical future values to highlight savings shortfalls.

But it’s really important to not lose sight of the risks of investing. Returns vary. In the case of common stocks, that variability means that in any given year, or over any given three-, five-, or ten-year period returns could actually be negative.

Also important is that past performance (while true and exact) shouldn’t be relied on as indicative of what may happen in the future. Your actual investment results will depend on a number of factors beyond your long-term asset allocation.

What to do Next

If you need help, call us at (800) 235-8396.

1 Including, but is not limited to, Markowitz, 1952; Brinson, 1986; Jahnke, 1997; Xiong, 2010; Harvey, Liechty, and Müller, 2010; Green, Hand, and Zhang, 2013; Ibbotson and Kaplan, 2020.

2 Òscar Jordà, Katharina Knoll, Dmitry Kuvshinov, Moritz Schularick, Alan M Taylor, (2019), The Rate of Return on Everything, 1870–2015, The Quarterly Journal of Economics, Oxford University Press, vol. 134(3), pages 1225-1298.