There is a third type of Individual Retirement Arrangement (IRA) with which you may not be familiar. It’s kind of a second cousin to the Traditional and Roth IRA. It has similar features to its better-known relatives but serves a much different purpose. It’s the Education IRA. And as its name implies, it isn’t intended to fund retirement at all. Commonly referred to as a Coverdell Education Savings Account (ESA), it may be an appropriate vehicle to finance future education expenses.

How a Coverdell is Like an IRA

There are some features that make the Coverdell ESA IRA-like. For example, your income determines your eligibility. And earnings get the same tax-advantaged treatment as a Traditional or Roth IRA.

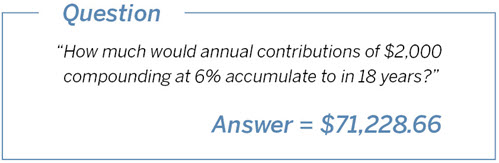

Investments in a Coverdell ESA can generate income and can grow free of federal income tax. If you live in a state that conforms to federal tax rules, then those earnings are not subject to state income tax either. But there are limits on how much money you can contribute to an ESA.

Contributing to an ESA

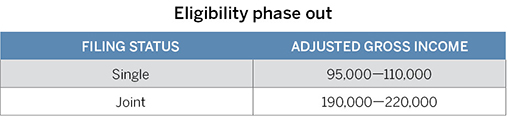

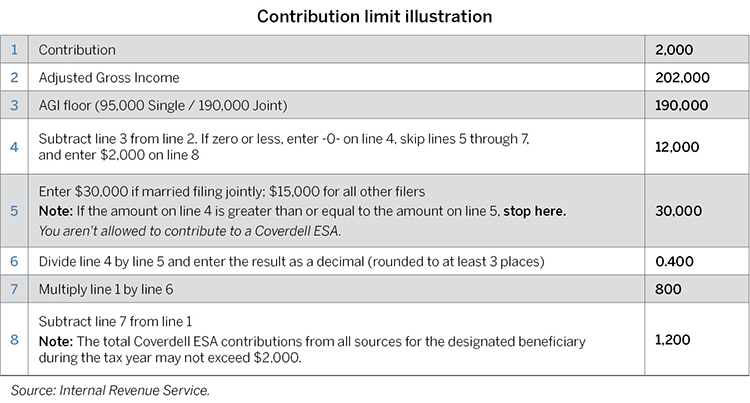

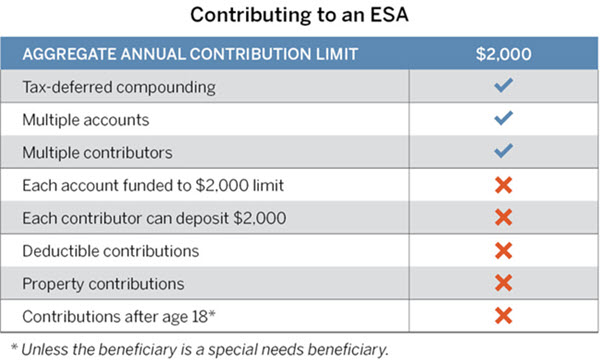

The maximum annual contribution is $2,000. And for some, it may not even be that high. Like its cousins, the education IRA phases out eligibility based on your income.

For example, a married couple making up to $190,000 can contribute the full $2,000 annually. Anything over that up to $220,000 a year and their contribution gets reduced. If they make more than $220,000, then they’re precluded from contributing to a Coverdell ESA. The numbers for a single taxpayer are half those of joint filers.

If you make more than the respective phase out limit, then you can gift money to someone who doesn’t and they can contribute to a Coverdell account for your child.

Anyone can. There’s no limit on how many people can contribute or how many separate accounts can benefit your child. The only limit is that the total of all contributions from all contributors in all accounts cannot exceed $2,000 a year.

Some of the Benefits of an ESA

In addition to tax-deferred earnings, there is no federal income tax on withdrawals used to pay Qualified Education Expenses incurred from kindergarten through 12th grade (at public, private, or religious schools) and on into college.

For primary and secondary school, qualified expenses include tuition and fees, books and supplies, computer equipment and software, internet access and related services, tutoring and transportation, uniforms and extracurricular activities, and room and board. Some of these are also qualified expenses when your children head off to college.

So, a Coverdell can be a strategic component of your overall college savings plan.

For example, accounts owned by grandparents or other relatives aren’t considered in the Expected Family Contribution (EFC) calculation when determining need-based financial aid. So, they won’t have an effect on initial awards. And even though withdrawals from those accounts are considered income, timing distributions may help mitigate their impact on future EFC calculations.

Other Considerations

ESAs are set up as trust or custodial accounts for children and contributions have to stop when beneficiaries turn 18.

Distributions that exceed qualified education expenses make the earnings portion of those withdrawals taxable income and subject them to an additional 10 percent penalty. This same treatment applies to any assets remaining in an account after a beneficiary reaches age 30.

To avoid the tax and penalty, funds can be transferred into the ESA of a family member under age 30 prior to the original beneficiary’s 30th birthday.

Contributions to an ESA can only be made in cash.

Any contributions over the $2,000 annual aggregate limit are subject to a 6 percent excise tax, which will continue to be levied each year the overage remains in the account.

Need More Info?

If you have questions about Coverdell ESA accounts, call us at (800) 235-8396.